Iraq Survey Group Final Report

Regime Finance and Procurement

Annex G

Iraq’s Banking System

Origins of the Iraqi Banking System

In imitation of Egyptian leader Abdul Nasser’s nationalist/socialist policies, the Iraqi government of Abd al-Salam ‘Arif nationalized all private commercial banks in Iraq in 1965, as well as the branches of foreign commercial banks. The government closed the nationalized banks and moved their customer accounts to the state-owned commercial bank, Rafidian Bank, which was owned by the MoF. As a result, Rafidian Bank had to rapidly expand its branch system to service its expanded customer base, but it did not have the human resources to manage a complex network. In addition, nationalization of the private banks caused the best bank managers to leave the industry and created distrust among foreign investors. The combined effect of these factors caused the effectiveness and service quality of the country’s banking system to deteriorate.

In response to Rafidian Bank’s inability to service the country’s banking needs, in the early 1970s the CBI and the MoF proposed to the government that a new state-owned bank be licensed. As a result, in 1988 Rasheed Bank, also owned by the MoF, was licensed. In addition to serving the private sector, Rasheed Bank and Rafidian Bank soon took over much of the banking business of state-owned enterprises, relieving CBI of that function.

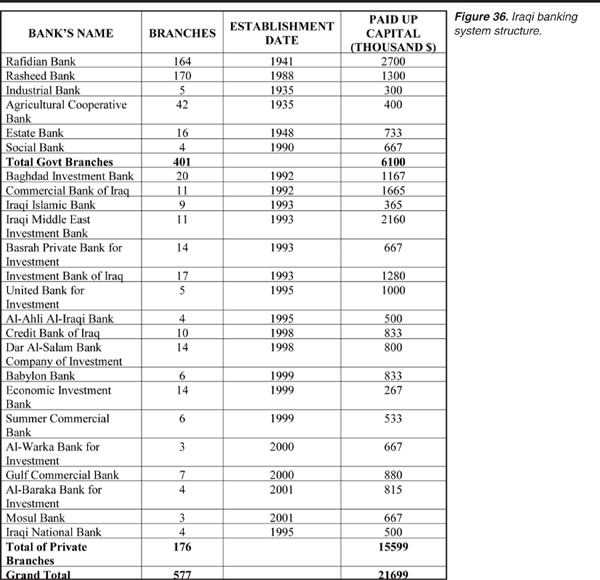

The Ministry of Finance was responsible for overseeing budgets of several ministries as well as the state-operated banking system. Currently, the six state-owned banks (Rafidian, Rasheed, the Agricultural, the Industrial, the Real Estate, and the Socialist) account for about 93 percent of banking system assets. There are also 18 private banks with capitalization of $25 million and deposits of $107 million.

The 18 private banks were established in an effort to handle local depositors’ financial needs and reform as well as modernize the banking sector. These banks remained small, in part because most Iraqis did not think it was safe to put their money in banks. Figure 36 lists both the state and privately owned banks of Iraq, including branches, establishment date and capital assets remaining after OIF.

{kind=link}

Organization of the CBI

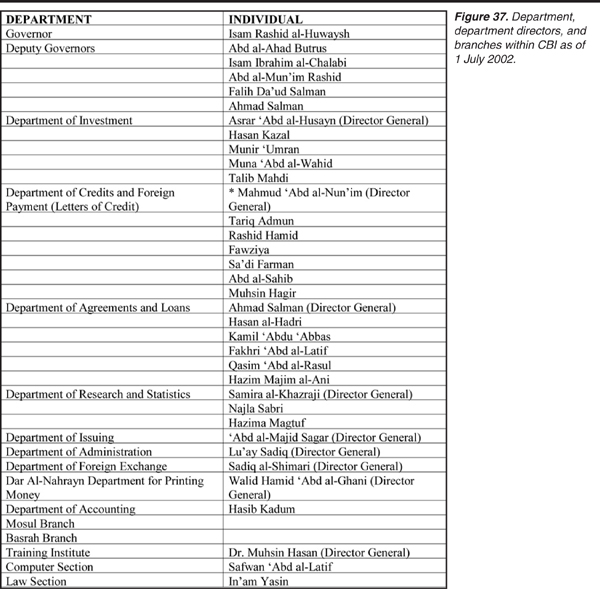

The CBI was composed of five main departments, plus support elements (see Figure 37).

{kind=link}

- Department of Investment. This department maintained account information for foreign accounts.

- Department of Accounting. This department maintained the employee accounts of the CBI.

- Department of Exchange. This department licensed money exchangers.

Iraqi Ministry of Finance’s Banking Role

The Iraqi MoF was headed by Hikmat Mizban Ibrahim al-Azzawi from 1995 to 2003. Azawi was responsible for managing the funds for the Iraqi government held in the CBI. All revenue for the government went into accounts in the CBI. Apart from normal budgetary requirements, a major duty for the Finance Minister was to disperse money for Saddam. The Presidential Diwan had special accounts separate from the normal government accounts. Routinely, letters from Saddam would arrive at the MoF ordering the transfer of funds from government accounts to Presidential Diwan accounts located at the CBI.

- The Presidency was also the authorizing authority for transferring money to other ministries. Any order for funds received by the MoF was sent to the Director of the CBI, Isam Rashid al-Huwaysh. Any disputes between al-Huwaysh and al-Azawi were settled by Saddam.

- When hard currency was collected in the CBI, it was allocated to the ministries that needed hard currency to buy things internationally, such as the Ministry of Health. Because hard currency was in such short supply, the ministries that received it had to pay it back in Iraqi Dinars.

The CBI did not make extra payments directly to any ministries or to the Diwan, including the IIS and the MIC. Payments were made to the MOF accounts at the Rasheed and Rafidian Banks, and then distributed. At the end of the month, the CBI would send an account of what was sent to the Rasheed and Rafidian Banks to the MoF. After two or three days the MoF would instruct the CBI to print Iraqi Treasury Bonds as an accounting procedure to balance the books. Iraq did not have a more formal economic or rigorous monetary policy.

State-Owned Banks

Iraqi had two state-owned commercial banks: the Rafidian and the Rasheed. Both the Rafidian Bank and the Rasheed Bank accounted for about $1.8 billion in assets, or about 86 percent of the total assets in Iraq’s banking system.

Rafidian Bank

The Rafidian Bank was owned by the Ministry of Finance and was founded in 1941. It was the largest, oldest, and most important commercial bank in Iraq. It handled much of the Regime’s foreign assets. The central branch of Rafidian bank was located in Baghdad. The chairman and General Manager was Diya’ al-Khayyun. In addition to the Baghdad Headquarters, there was a main branch in Basrah; and over 164 smaller branches located throughout Iraq. There were eight overseas branches in Bahrain, Egypt, Jordan (2), Lebanon, United Arab Emirates, Yemen, and Great Britain.

Rafidian Bank was primarily a conduit for transferring money out of Iraq. Several branches were involved in passing illicit revenue from oil and cigarette smuggling around the Middle East. In the February to April 2002 timeframe, Mufid ‘Aziz (Director of Rafidian Bank) and ‘Abd al-Huwaysh all-Mukhtar (Regional Director of the Rafidian Bank) withdrew $50 million from accounts at the Commercial Bank of Syria.

Rasheed Bank

The Rasheed Bank was Iraq’s second largest commercial bank with 170 domestic branches. It was government-owned and established in 1988. It operated outside Iraq through correspondents. The Rasheed Bank was established to provide competition for Rafidian, primarily in Iraq.

Specialized Credit Banks

Iraq also used four specialized state-owned banks: the Agricultural Bank, the Industrial Bank, the Real Estate Bank, and the Socialist Bank, all which collectively account for about seven percent of the total assets in the banking system. These four banks were established to increase the flow of financial support to certain sectors of Iraq’s economy such as agriculture, industry, business creation, and real estate. They played virtually no role in Iraq’s illegal financial transactions during sanctions.

Privately Owned Banks

In the face of decreasing foreign currency reserves held in country and an increasing illiquid domestic banking system, the CBI and MoF in approximately 1992 successfully petitioned the government to allow the licensing of new private commercial banks. By February 2003, there were approximately 18 private commercial banks. These private banks offered superior service, were more computerized, and were faster growing than the state-owned banks. By early 2003, the private banks held the majority of private-sector accounts and deposits, although the government ministries and state-owned enterprises still banked primarily with state-owned banks.

Private banks were set up with capital from individuals. Under Iraqi banking laws, no one individual was allowed to own more than a five-percent share holding in a private bank. The quality of management of the private banks was better than the government-managed banks. The private banks were able to offer better salaries, and attract the best candidates from the banking sector.

According to a senior Iraqi Government official, in order to evade controls under international sanctions, the government of Saddam used private commercial banks for some transactions in the belief that private banks would not be as closely monitored by the UN as the state owned banks and the CBI.

Middle East Bank

Uday Saddam Husayn al-Tikriti owned shares in the Middle East Bank. The Middle East Bank is one of the largest private banks in Iraq. Uday also controlled the appointees and directors of the bank.

Islamic Bank

The Islamic Bank was unconventionally established. Formed by the Humayim family, the bank was established on a decree from the RCC, which was contrary to Iraqi banking rules and regulations. Money of Ba’ath Party Members and supporters of the Regime was deposited into this bank.

The Role Played by the Hawala System

The hawala system was the most common informal payment system used in Iraq under Saddam. The Iraqi Regime encouraged its citizens in Iraq and abroad to open accounts in foreign currencies at Iraqi banks in order to track funds that were traditionally transferred through informal payments arrangements. The reliability of the ancient hawala system came from trust and the extensive use of personal connections and family-tribal relationships. In its simplest terms, an individual desiring to transfer money exchanged cash for a hawala note, often coded or secretly marked to foil potential counterfeiters. This note would then be transferred to the other party via mail or courier. The party on the other end of the transaction then presented the note to an associated exchanger in their country, who converted the hawala note back into the appropriate cash specified in the note, minus a handling fee. In modern times, the use of e-mail, faxes, and telephones have made these private cash transfers almost instantaneous and nearly impossible to trace or regulate.

Before OIF, there was no regulation of the hawala system in Iraq and the use of them was outlawed. Regardless, illegal hawalas were often used by the average Iraqi individual or company to transfer funds from expatriate communities to the homeland. The illicit system is reliable and efficient and is preferred because it is faster and less expensive than bank hawalas.

- The speed is due to the lack of paperwork and bureaucracy, while the cost effectiveness is due to not having to deal with a bank’s artificial, higher exchange rates. However, the anonymity and lack of traceable documentation make this system vulnerable to abuse by individuals and groups transferring funds to finance illegal activities.

- For example, in order to import goods, a letter of credit was normally needed from a bank in Jordan. To get this, the Jordanian bank would need some cash. Because it was illegal to transfer cash out of Iraq through the normal banking system, the illegal hawala system was used to move the money.

- The hawala system was positive for the economy because it reduced the liquid cash within the economy and helped counter the effects of inflation. Hawalas were eventually legalized and regulated by Saddam in an attempt to reduce smuggling and help stimulate the economy.

The Hawala

The term “hawala” means “transfer” or “wire” in Arabic banking terms. The word hawala comes from the Arabic root hwl, meaning to “change” or “transform.” In common Arabic usage, hawala are performed in three different ways—two of which are legal:

- Hawalas through Iraqi banks are synonymous with bank money transfers. Bank hawalas are legal.

- Illegal hawala transfers are based on an ancient informal banking system used throughout South Asia and the Middle East to transfer money across distances past legal and financial barriers. In modern times, unlicensed money exchangers use this process, coupled with modern telecommunications to discreetly transfer money.

- Hawalas made using the old process via licensed money exchangers are considered legal. Not all money exchangers perform hawalas.

|

NEWSLETTER

|

| Join the GlobalSecurity.org mailing list |

|

|

|