Business Aviation

Business Aviation is one of the largest in terms of hours flown. Business aviation is the use of a private- or company-owned general aviation aircraft for business purposes. Business aviation is usually divided into two groups according to who is flying the aircraft. If an individual personally pilots an aircraft used by a business in which he or she is engaged, it is classified as a business aircraft. If on the other hand, a professional pilot flies a company or corporate aircraft to transport employees and/or property, the airplane is classed as an executive aircraft.

Business jets are turbojet aircraft weighing less than 100,000 pounds maximum gross takeoff weight, with wingspans less than 100 feet that are used by companies to conduct their business. Such Light Jets typically seat fewer than 30 passengers and are designed primarily for executive transportation. This includes company jets, privately owned jets, and jets employed for air taxi services. Unlike large commercial aircraft and regional jets, LJs provide point-to-point transportation to virtually any airport. Additionally, LJs are not subject to the scheduling constraints imposed by commercial air carriers, or the delays inherent with ticketing and TSA security screening. Catering to high-end customers, LJs offer a convenient means of air transportation for those who can afford it.

The LJ market is experiencing a period of high demand. In the U.S. alone, more than 10,000 companies own private planes - nearly double the number in the 1990s. Given the increasingly global nature of business enterprises and the demands for business travel, this trend is likely to continue. Demand for LJs will continue to rise and are adjusting their business strategies accordingly. Given the rapid growth of VLJs and the forecast for continued expansion, there are concerns that an already overtaxed air traffic infrastructure may not be able to accommodate all the extra aircraft. In addition, major airlines contend that it costs just as much to land a VLJ as it does a large airplane, yet private aviation pays only a fraction of the cost to maintain the air traffic system despite the fact that private aviation (including VLJs) represents the bulk of airplane traffic in the US. It is likely that major airlines will lobby to have private aviation pay a large share of the planned modernization of the air traffic control system. If these arguments are successful, LJ operating costs will likely increase.

With the successful introduction and acceptance of commercial jet transports it was only a question of time until the performance potential of turbine power was applied to the general aviation airplane. The origin of the businessjet can be traced to the four-place, French built Morane-Saulnier MS760, which first flew in mid-1954. However, a 1955 attempt by Beech Aircraft to market this alrplane in North America can best be described as unsuccessful. The next airplane to enter the small jet transport arena was the Lockheed Jetstar, with the original twln-englned prototype flying in September 1957. The Jetstar was orlglnally designed for the military market in response to the UCX program for a small jet transport with the eventual outcome of this effort being the four-engined C-140.

The next airplane to come along was the North American Sabreliner flying in September 1958, as an entry into the military UTX competition for a trainer category airplane. The third small transport took to the air in February 1959, when the four-engined McDonnell Model 220 flew, with this airplane also competing for the UCX contract. In the final analysis, the Jetstar won the UCX race, the Sabreliner took the UTX contract and McDonnell dropped the Model 220 program.

When corporate jets first flew onto the market, most businessmen were reluctant to buy such expensive gadgets for fear of irritating cost-conscious stockholders. But improvement in corporate profits and the introduction of new and cheaper jets soon allayed much of that fear. By the early 1960s many a corporate president believed that a rakish new jet is just what his company needed for greater mobility and smarter image. The executive jet was well on its way to gaining the acceptance already won by its piston-engine counterpart.

The next period of activity in this field took place in 1962, when the first deHavilland DH 125 flew. The following year, 1963, produced a bumper crop of airplanes with the first flights of the Jet Commander, the French designed Mystere 20, and the Lear Jet taking place. The swept-forward wlng German Hansa Jet and the Italian PD808 made their first flights in 1964. A new era in blg business jets began when the Grumman Gulfstream II made its initial flight in 1966. The next business jets to join the field include the Cessna Citation, the Falcon 10, and the Corvette.

All of these business jets (with the exception of the MS760 and the McDonnell 220) were of the aft fuselage mounted engine configuration. While the large commercial transports and the smaller business jets were similar in configuration, there is a difference between the two designs. Specifically the aft-engined transport aircraft tend to have the nacelles located well aft of the wing trailing edge, for example the DC-9 and 727. In the case of the smaller airplanes, the nacelles are located quite close to the wing and in several designs the nacelles overlap the wing. Because of the proximity of the nacelles to the wing, the business jet offers same challenging design problems in terms of achieving a minimum drag configuration. Also, the trend in business aircraft design has been towards the incorporation of high bypass fan engines. These engines, with their larger physical size, make it very difficult to arrive at a wing mountedenginearrangementthat is compatible with a high performance business jet design. Thus, the aft-engined airplane appears to be a viable configuration in the years ahead.

The executive aircraft is usually larger and more luxurious than the business aircraft. The majority are multi-engine and one-third are jet powered. In general, they are used to carry very important people over medium-length distances in comfort and at relatively high speeds. To these people, time means money and getting them to their destination in the minimum amount of time is very important. There are over 55,000 aircraft in the business aviation category. The vast majorities of the business aircraft are single-engine piston aircraft. About 33 percent of the executive aircraft are either turboprop or turbojet powered. In the business aircraft category, only about one percent are turbine powered. Looking at these figures, there are some generalizations that can be made. A typical executive transport is a twin-engine aircraft and is almost as likely to be turbine powered as piston powered.

These types of aircraft are in areas where the pilot must have special training, a multi-engine rating and at least a commercial license. If the aircraft is turbine powered, another rating is required. These executive aircraft are also very expensive, as we shall see later. On the other hand, the typical business aircraft is almost certain to be piston powered and is three times as likely to have a single engine as twin engines.

The typical business aircraft is similar to the typical personal aircraft in that it is a single-engine, four-place airplane. However, the business aircraft is probably better equipped. Because it is important in some businesses to be able to fly even in bad weather, the typical business airplane is well-equipped with instruments. Almost all business aircraft pilots are instrument rated.

There are three areas of concern in aviation today, and they play an important part in the decision of which aircraft to buy for use in a business. These three areas are (1) fuel efficiency, (2) noise and (3) cost effectiveness. Weight, engine size and speed affect the fuel efficiency of the airplane. The main reason for using an airplane for business is to save time. If a business airplane can get executives to a business meeting faster than the commercial airlines, the money saved in terms of salaries justifies the travel. The Federal Government placed limitations on the amount of engine noise an aircraft can produce. Many communities close their airports to jets at night. These restrictions are for environmental reasons and are getting more severe. The aircraft manufacturers are building quieter jets, and many businesses are turning to these quiet aircraft.

In the past, many businesses bought aircraft based on speed plus the length of the longest trip their employees traveled. This led to aircraft that were underutilized. For example, if a company makes only one 2,000-mile trip a year and all the rest are only 300 miles, that company really doesn't need an airplane with a 2,000-mile range. It would be better to buy an airplane with a 500-mile range (which would be cheaper) and use the airlines for the 2,000-mile trip. For instance, a twin-engine turboprop aircraft can make a 500-mile flight in 2 hours 15 minutes, while a turbojet can make the same flight in 1 hour 50 minutes. The turbojet saves 25 minutes on the flight. However, it costs a great deal more to buy and it burns 600 gallons more fuel on the trip.

The executive aircraft market is a very competitive business. Many manufacturers, both US and foreign, are building high-quality aircraft to meet the needs of today's corporations. The largest and most successful of the US corporations own and operate a sizable fleet of very expensive aircraft. Since these companies are very cost conscious, they must have determined that business aviation helps them make money.

There are many fine turbocharged-, twin-, and piston-engine aircraft that are not pressurized. The only disadvantages to these unpressurized aircraft are in passenger comfort and speed. The unpressurized aircraft cannot fly as high as pressurized ones and this means a bumpier ride. Also, the unpressurized aircraft causes more ear discomfort when climbing and descending.

The next step above the largest piston twin is the turboprop twin. The big difference between them is in the power plants. The largest piston twins have engines of about 375 to 400 horsepower. The turboprops have engines rated as high as 850 horsepower. This increase in horsepower offers two advantages, the aircraft can be larger and fly faster. This is the major selling point for the turboprop executive aircraft. It isn't until you get beyond the range of the piston-engine twins that the turboprops begin cutting time off trips. It will actually take a turboprop a little longer to make a 500-mile trip than a pistonengine twin. This is because it takes longer to climb to the higher cruising altitude of the turboprop. However, on a trip of 1,000 miles the turboprop will save a lot of time because the piston-engine twin will have to stop for refueling. On the other hand, the price of a turboprop is much higher; in most cases, nearly three times as much as the most expensive pressurized twin. They will have to decide if there are enough long trips with several passengers to justify the additional expense of a turboprop.

Some of the twin-engine turboprop aircraft are large enough that they are widely used by the commuter airlines.

Turbojets are often called bizjets, or corporate jets, and are the top-of-the-line for executive aircraft. A corporate jet is expensive to buy and to operate. Even the smallest bizjet will burn over 100 gallons of fuel per hour and larger ones can burn almost 300 gallons per hour.

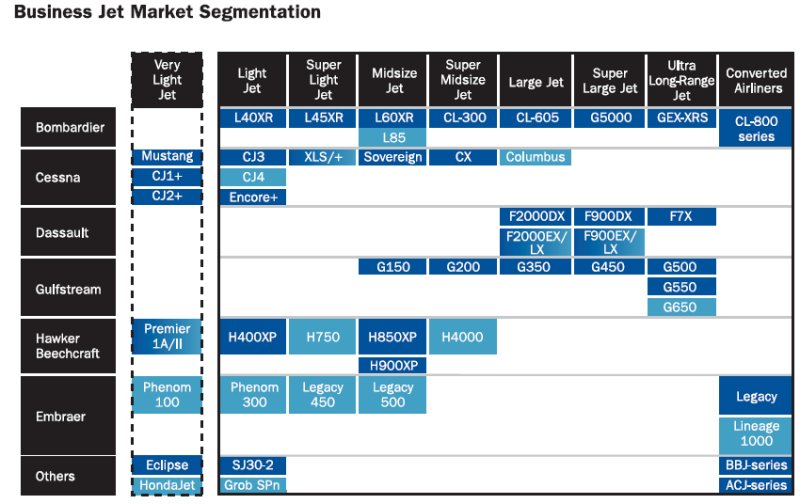

There is quite a bit of difference in the amount of room inside the cabin of the various business/ executive jets. In most of them, the dimensions are about 5 feet wide by a little over 4 feet high. You can see that it would be very difficult to get up and walk around in a cabin this size. There are some that are considerably more roomy, and the trend is toward larger cabins. This leads to larger engines and more fuel consumption. The result is that there are classes of business/executive jets small (Learjet, Citation, etc.) and large (Gulfstream, Jetstar, etc.). The cost of the aircraft also goes up as the size increases.

The 2001-2003 downturn was caused by various coinciding factors. The high percentage of aircraft for sale on the pre-owned market at the end of the 1990s was the first sign of the market slowdown. In the U.S., conjectural factors like the slowdown of the economy and the fall of corporate profits at the end of 2000 and in 2001 considerably reduced the demand for business jets. Business aviation may have also suffered, although likely to a smaller extent than commercial aviation, from the climate of uncertainty following 9/11. The reduction in the overall number of gross business jet orders, coupled with significant cancellations both from traditional and fractional businesses, forced Original Equipment Manufacturers (OEM) to sharply reduce production.

The U.S. economy regained its momentum, and the demand for business jets rose between 2004 and 2007. Previously untapped markets in Europe, Asia and the Middle East were starting to generate substantial demand. Moreover, OEMs launched many new models in recent years, pushing orders even higher. The 798-unit delivery record set in 2006 was broken in 2007, with deliveries totalling 863 units for the year.

At the end of 2007, the worldwide fleet was estimated to be approximately 12,800 aircraft for all segments excluding the Very Light Jet segment. With a yearly retirement rate of 0.5% to 1% of the fleet and expected deliveries, the business jet fleet could grow to approximately 24,800 aircraft in 10 years. This impressive growth could put pressure on pilot training, maintenance facilities and aviation infrastructure. With over 70% of the worldwide business jet installed base, the U.S. remains the single most important market for manufacturers. The U.S. business jet demand pool is mostly driven by wealth creation.

While the U.S. business jet market remained on a growing mature trend, with a healthy mix of repeat purchases and concept buyers, the international market gained momentum due to the surge of the Western European market and the emergence of a new cohort of customers in non-traditional markets such as Russia and Eastern Europe. Although the world GDP was fuelled by double-digit growth, by early 2008 the economic environment was at a turning point as the U.S. economy cooled. Despite a recession in 2008 and 2009 that could lead to a decrease in orders, industry trends will sustain market deliveries for the next 10 years above the new level that was reached in 2007. Over this period Bombardier forecast deliveries of 13,200 aircraft in the segments in which it competes, generating an industry total of $300 billion in revenues, compared to 6,200 aircraft and $117 billion in total revenues during the previous 10 years.

|

NEWSLETTER

|

| Join the GlobalSecurity.org mailing list |

|

|

|