ANNUAL REPORT TO CONGRESS

Military Power of the People's Republic of China

2006

Military Power of the People's Republic of China

2006

Chapter Four

Resources for Force Modernization

Resources for Force Modernization

military and civilian scientific-technological resources, and that organically integrates

basic research, applied R&D, product designing and manufacturing, and procurement of

technologies and products so as to create a good structure under which military and civilian

high technologies are shared and mutually transferable."

- President Hu Jintao, January 9, 2006

Overview

Sources for PLA force modernization include domestic defense expenditures, foreign acquisitions, and indigenous defense industrial developments - all of which are driven by the performance of the economy. China's impressive economic growth has enabled Beijing to make ever-higher investments in the defense sector. Real growth of China's official defense budget, for example, has averaged double-digit annual growth every year for the past decade. The official budget does not account for hidden assets and off-budget revenues and therefore does not give a full picture of actual military expenditure.

As its domestic defense industry matures, China is actively seeking foreign weapons and technology, primarily from Russia and states of the former Soviet Union, to fill near-term capability gaps. In the long term, however, Beijing seeks to establish a wholly indigenous defense industrial sector. China's military industrial base also benefits from foreign direct investment and joint ventures in the civilian sector, the technical knowledge and expertise of students returned from abroad, and industrial espionage. The EU arms embargo is a critical issue in this context. The ban remains an important symbolic and moral restraint on EU countries' military interactions with the PLA. Lifting the embargo would potentially allow China access to military and dual-use technology for improving current weapon systems and developing indigenous capabilities to produce future systems.

Seeking Sustainable Growth

China's economy has witnessed tremendous growth since reform and opening began in 1978. Linear projections of China's economy show real GDP growth through 2025 to $6.4 trillion. However, these linear projections assume the absence of natural disasters, limited domestic social disruption, and access to sufficient resources. Taking these into account, China's economy is expected to grow at a somewhat reduced rate in the future (5.8 percent real growth over the next 20 years compared to 8.6 percent over the past 20). Comparatively, in 2025 Russia's GDP is projected to be $1.5 trillion, Japan's $6.3 trillion, and the U.S., $22.3 trillion.

The rapid development of China's coastal regions has produced numerous social problems, including growing economic inequality. A January 2006 article co-authored by the Commander and Political Commissar of the paramilitary People's Armed Police (PAP) notes, "the uneven character of economic and social development . . . and contradictions among the people [have resulted in] growing numbers of group incidents . . . [that have been] difficult to handle."

China's financial system has not kept pace with the economy, leaving many unsustainable and insolvent institutions. State-owned enterprises have been a major drag on the economy, but their elimination would reduce social services available to workers. Furthermore China's "One-Child" policies have undermined the traditional Chinese dependence on large families for social support. As the average age of China's population starts to rise, the problem of caring for the elderly will become more burdensome. The failure to deal adequately with any or all of these challenges could put a brake on economic expansion.

To address these concerns Party leaders constructed the 11th Five-Year Plan (2006-2010) to promote balanced and sustainable economic growth. Under the plan China's leaders intend to revitalize the northeast "rust belt;" encourage coastal provinces to concentrate on advanced technology; expand the service sector; and shift economic activity to the northeast, central, and western provinces where new urban centers will be created. This ambitious redistribution could strain central government coffers and affect funding for the PLA.

Military Budget Trends

Since the early 1990s, China has steadily increased resources for the defense sector. On March 5, 2006, a spokesperson for China's National People's Congress announced that China would increase its publicly disclosed military budget in 2006 by 14.7 percent, to approximately $35 billion. The 2006 increases continue a trend of double-digit increases in China's published figures that has prevailed since 1990. When adjusted for inflation, the nominal increases have produced double-digit actual increases in China's official military budget every year since 1996. However, the officially published figures substantially underreport actual expenditures.

DIA estimates that China's total military-related spending will amount to between $70 billion and $105 billion in 2006-two to three times the announced budget. At the top end, this represents a figure for spending more than twice that of Japan. If China maintains a relatively constant defense burden - proportion of GDP devoted to defense expenditures - nominal total defense spending could rise three-fold or more by 2025, based on current economic projections.

Determining Actual Military Expenditures

The lack of detail in public Chinese military expenditure data is an outgrowth of a political system in which military spending, along with other aspects of military posture, is treated as a state secret. While the United States has long urged China to increase transparency in reporting military budgets and expenditures, to date Beijing has only provided a highly aggregated breakout of maintenance and operations, personnel, and equipment roughly defined as equal shares in its Defense White Papers.

What little public information China releases about defense spending is further clouded by a multitude of funding sources, subsidies, and cutouts at all levels of government and in multiple ministries. Real spending on the military, therefore, is so disaggregated that even the Chinese leadership may not know the actual top line. The Intelligence Community assesses the following additional funding streams not reflected in the official military budget are used to support China's armed forces: Foreign weapons procurement, sales, and aid. Foreign weapons purchases are funded directly by the State Council and are often negotiated on commercial terms. The revenues generated by arms sales primarily go to military industries, but the PLA receives a small commission on new sales and sales of used and warehouse stocks. China averages approximately $600 million in arms sales annually.

- Paramilitary (People's Armed Police) expenses. The People's Armed Police (PAP) is funded from the Ministry of Finance and the Ministry of Public Security, although some sources indicate it is partially paid for out of Ministry of State Security accounts. Ministries employing PAP personnel and localities with PAP units also provide funding. The PAP earns additional funding from economic activities including mining and agriculture, as well as fines and fees from its security activities.

- Strategic Forces. The PLA Second Artillery Corps is the only service with its own budget. Some analysis indicates that it also likely receives some direct funding from the State Council outside the announced military budget.

- State subsidies for the military-industrial complex. Military factories under the General Armament Department (GAD) receive direct state allocations for converting factory use between civil and military products. Machinery upgrades for civilian production are often intended for improved military production. Weapons production costs are thus partially defrayed by State Council subsidies, rather than funded wholly through the military budget. Military-related industries are also encouraged to develop and produce civilian products to reduce overhead and reliance on government subsidies.

- Military-related research and development. Funding sources for military research and development include direct allocations from the Commission of Science, Technology and Industry for National Defense (COSTIND), GAD, the Ministry of State Science and Technology, the industries themselves, research institute selffinancing earnings, local government funding, and others. More than 80 percent of government science and technology appropriations are not associated with overt government-sponsored programs, making it difficult to account for expenditures in military-related activities.

- Extra-budget revenue. PLA divestiture of commercial enterprises in the late 1990s did not affect the PLA's traditional production enterprises (e.g., farms and uniform/materiel manufacturers). Other sectors, such as transportation and telecommunications, were exempted. Almost 3,000 commercial firms belonging to the PLA and PAP were transferred to local governments and some 4,000 others were closed, but 8,000-10,000 enterprises continue under PLA direction.

Foreign Weapons and Technology Acquisition

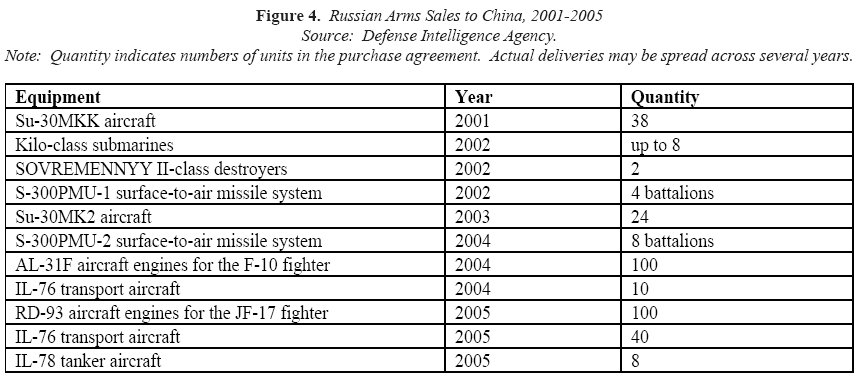

According to currently available data, China signed arms agreements with suppliers worth almost $13 billion from 2000-2005, with deliveries during this period estimated at $11 billion. Russia alone provided approximately 95 percent of arms sold to China in the last decade and remains China's chief supplier of weapons and materiel.

Beijing's purchase of advanced Russian weapon systems available for export has included Su-27 and Su-30 fighter aircraft; AA-12 airto- air missiles (AAMs); SA-10, SA-15, and SA-20 surface-to-air missile (SAM) systems; 3M-54E (SS-N-27B) ASCMs; KILO-class submarines; SOVREMENNYY II-class destroyers; IL-76 transport aircraft, IL-78 tanker aircraft; and associated weapon systems.

China also relies on critical Russian components for several of its weapon production programs and, in some cases, has purchased the production rights to Russian weapon systems. Russia continues to cooperate with China on technical, design, and material support for numerous weapons and space systems.

Russia has historically refrained from transferring its most sophisticated weapons systems to China. However, China's persistent pressure on Russia to make available more advanced military equipment - particularly using Russia's dependence on Chinese arms purchases as leverage - could cause a shift in Sino-Russian military cooperation.

In addition to Russia, Israel has also been a supplier of advanced military technology to China. Although Israel began the process of canceling the PHALCON program with China in 2000, Beijing is working to complete the development of an AWACS variant built on an IL-76 airframe. The Israelis transferred HARPY UAVs to China in 2001 and conducted maintenance on HARPY parts during 2003-2004. In 2005, Israel began to improve government oversight of exports to China, strengthening its controls of military exports and establishing controls on dual-use exports. These improvements will require legislation by the Knesset, re-organization within the Israeli Ministry of Defense, and enhanced roles for its Ministry of Foreign Affairs and Ministry of Industry, Trade and Labor.

Military Industries and the Science and Technology Base

Most of China's defense industries rely on foreign procurement and development. The exceptions are few, e.g., ballistic missiles and some space and aviation programs.

Civilian industrial reform has advanced more quickly than the military sector because it can attract foreign investment with fewer restrictions. However, foreign investment in physical plant, management, technical, and marketing expertise in some basic manufacturing sectors, such as strategic metals and electronics, has increased the prospect for spin-off with military and dual-use industries. Joint ventures in China also now manufacture semiconductors and integrated circuits used in military computers, communications and electronic warfare equipment, and missile guidance and radar systems.

Many of China's new generation of scientists, engineers, and managers receive training and have experience in the United States and other countries. In 2004, the United States granted 35,578 F-1, J-1, and M-1 student or exchange visas to PRC nationals, according to the Department of Homeland Security, Office of Immigration Statistics.

China also continues to acquire key technologies and manufacturing methods independent of formal contracts. Industrial espionage in foreign research and production facilities and illegal transfers of technology are used to gain desired capabilities. Where technology targets remain difficult to acquire, foreign investors are attracted to China via contracts that are often written to ensure Chinese oversight, with the eventual goal of displacing foreigners from the companies brought into China.

China's primary military industry weaknesses have been the relative lack of scientific and engineering innovation, bloated bureaucracy, and poor business practices - all issues now receiving considerable attention. In a move to increase innovation through competition, the PLA recently announced it will award permits to private institutions and foreign enterprises for R&D in weapons and equipment.

Lifting the European Union Arms Embargo

The European Union (EU) arms embargo on lethal weapon sales to China was imposed following the PRC's 1989 crackdown on Tiananmen Square demonstrators. The embargo is a political commitment subject to interpretation by EU members. Beijing has mounted a diplomatic campaign to lift the ban, offering special incentives for foreign investors and the lure of strategic partnerships. Even without incentives, EU defense industries face a shrinking global marketplace and regard China as an attractive source of potential business.

Although the EU has stated that lifting the embargo would result in no qualitative or quantitative increases in China's military capabilities, the EU's tools to enforce such a commitment remain inadequate. Lifting the embargo would potentially allow China access to military and dual-use technologies that would help it improve current weapon systems. It would additionally allow China to improve indigenous industrial capabilities for production of future advanced weapon systems. Ending the embargo could also remove implicit limits on Chinese military interaction with European militaries, giving China's armed forces broad access to critical military "software" such as management practices, operational doctrine and training, and logistics expertise.

If the embargo is lifted, China's strategy would likely center on establishing joint ventures with EU companies to acquire expertise and technology. China can be expected to move slowly to avoid undermining its position that the embargo was merely a "Cold War relic." Even if China were to move quickly, its defense industries would require time to integrate new technologies, processes, and know-how into weapons manufacturing or retrofits. In the medium to long term, however, China is likely interested in acquiring advanced space technology, radar systems, early-warning aircraft, submarine technology, and advanced electronic components for precision-guided weapons systems.

Lifting the EU embargo would also lead to greater foreign competition to sell arms to the PLA, giving Beijing leverage over Russia, Israel, Ukraine, and other foreign suppliers to relax limits on military sales to China. Potential competition from EU countries already may have prompted Russia to expand the range of systems it is willing to market to China.

Finally, lifting the EU arms embargo could accelerate weapons proliferation to countries that the EU wants to remain isolated. Beijing's track record in transfers of conventional arms and military technologies suggests EU or other thirdparty sales to China could lead to improvements in the systems that Chinese companies market abroad, including to countries of concern. Of note, some of China's major recipients of military assistance - Iran, Burma, Sudan, and Zimbabwe - are all currently subject to EU arms embargoes.

|

NEWSLETTER

|

| Join the GlobalSecurity.org mailing list |

|

|

|