Regional Turboprop Aircraft

|

|

Air service from small cities to congested or slot constrained hub airports is an important market for the commuter turboprop airplanes which provide most of this feeder service. A major irony of the jet age is that most of the time spent in airline travel is on the ground. For airline trips under 700 miles or so, passengers spend over one-half their total journey's time on the roads surrounding airports, at the terminal, and in the aircraft while it taxis and waits for takeoff clearance or an available gate after landing.

These commuter airlines came into existence in the 1960s. When the major carriers began buying larger jet-powered aircraft, they found they could not economically serve many of the small communities. In some cases, the airports in the small communities could not handle the heavier and faster jet aircraft. The Civil Aeronautics Board allowed the major carriers to leave these small cities to the commuter airlines. This ensures that the smaller communities will continue to have air service, but allows the larger carriers to get out of an unprofitable market.

Passenger air service to the small American communities had declined steadily since 1960, as the Civil Aeronautics Board (CAB) allowed first the trunks and then the local service airlines to withdraw from short-haul, low-density markets. Between 1960 and 1978, 187 small- and mediumsize cities were dropped from regulated airline routes. Even before 1978, the certificated airlines had been replaced in many markets by unregulated, unsubsidized commuter airlines, whose smaller aircraft and lower operating costs were better suited to short-haul, low-density air service.

In 1978, the US Congress deregulated the airline industry, phasing out the federal government's control over domestic fares and routes served and allowing market forces to determine the price, quantity, and quality of service. The Airline Deregulation Act of 1978 was good for the regional-commuter carriers. As the larger airlines dropped their less profitable routes, the regionals moved in to provide service.

Most legacy carriers, free to determine their own routes, developed "hub-and-spoke" networks. These carriers provide nonstop service to many spoke cities from their hubs. The airports in the small spoke communities include the smallest airports in the nation's commercial air system. Depending on the size of those markets(i.e., the number of passengers flying nonstop between the hub and the spoke community), the legacy airlines may operate their own large jets or use regional affiliate carriers to provide service, usually with regional jet or turboprop aircraft.

For purposes of the Federal Aviation Administration (FAA) forecasts, air carriers that are included as part of the regional/commuter airline industry meet two criteria. First, a regional/commuter carrier flies a majority of their available seat miles (ASMs) using aircraft having 70 seats or less. Secondly, the service provided by these carriers is primarily regularly scheduled passenger service.

The current small package express market was virtually nonexistent prior to 1980. Today, major integrated air carriers, who also act as charterers and forwarders such as Federal Express, UPS, DHL, and others ship millions of packages for next- and second-day delivery all over the U.S. This has generated a major (and continuing) demand for "air feeder" service, in airplanes that transport packages delivered to major hubs by the parent carriers' large jet freighters, to smaller outlying communities in the morning. These same airplanes then carry packages shipped from the smaller communities back to the hubs in the evening, where they are loaded aboard the large jet freighters, flown to sort centers such as Memphis (FedEx), Louisville (UPS), and Cincinnati (DHL) for overnight sorting and redistribution. Similar growth has been experienced in U.S. Postal Service, air courier, and financial document transportation requirements.

The original commuter fleet in the 1960's consisted of single-engine and light-twin aircraft that had low initial costs but few passenger amenities. As the industry grew, the carriers began to operate commuter derivatives of more modern executive aircraft; but CAB still restricted commuters to aircraft of no more than 12,500 lb-between 15 and 19 passengers. This meant that there was little domestic market for larger commuter aircraft, and even when CAB raised the limit to 30 passengers in 1973 many commuters preferred to stay with the smaller aircraft. As a result, no U.S. manufacturer developed a new aircraft in the 20- to 30-seat range, and the new foreign aircraft that were available captured most of the market. Deregulation raised the size limit to 60 seats, and once again those carriers who wanted to up grade their fleets had no modern U.S. option: they could buy the one new foreign aircraft that was available, or settle for older piston or twin turboprop aircraft - many of them also foreign made- of the type once flown by the local service airlines.

New technology has been one of the major factors in the commuter industry's growth. The industry has traditionally used small 19 to 30 seat propeller-driven (both piston and turboprop) aircraft to move their passengers to and from the hub airports served by major airlines. Passengers were not fond of these aircraft because of their relatively cramped cabins, loud interior noise levels, and safety record, particularly compared to jet aircraft such as the B-737. The airframe manufacturers noted the inherent problems with small turboprop aircraft (Beech 1900, DH Twin Otter, etc.) and developed larger and quieter turboprop aircraft to meet the growing demand for larger aircraft by the commuter operators.

American manufacturers never developed a dedicated aircraft specifically for commuter use. In large part this is a lingering effect of the commuter industry's regulatory history (the Civil Aeronautics Board (CAB) 10,000-lb weight limit for air taxis in 1947, the 12,500-lb limit for commuters in 1969) and the industry's indecision when the limit was raised to 30 seats in 1973. These factors effectively killed the domestic market for commercial aircraft between the largest the commuters were allowed to fly (19 seats) and the smallest the local service airlines wanted to fly (60 to 75 seats). In addition, the commuter aircraft market was extremely diversified, ranging from the smallest 4-seaters to the 19-seat limit, and was made up of numerous small companies that bought only one or two aircraft apiece. Manufacturers and other observers also cite the costs and uncertainties involved in Federal Aviation Administration (FAA) certification for newtechnology aircraft. As a result, the U.S. aircraft in use by the commuters was developed primarily as passenger derivatives of more lucrative general aviation and business aircraft designs.

Other manufacturers outside the United States, on the other hand, continued to design and build new dedicated passenger aircraft in the 15- to 20-, 30- to 35-, and 50- to 60-seat ranges for the European and Third World markets, frequently with government subsidies. They consequently had a considerable competitive advantage when CAB raised the commuter size limit to 30 passengers in 1973. U.S. manufacturers, apparently still considered the market too small and/or too risky. Similarly, when deregulation raised the commuter capacity limit to 60 passengers in 1978, the only American aircraft in the market were 20-year-old local service aircraft that were no longer in production. Other manufacturers, on the other hand, could offer the new 50-seat Dash 7 as well as older but serviceable aircraft like the BAe HS-748 and Fokker F-27, which had been upgraded over the years and were still in production.

The fundamental character of the American regional/ commuter industry changed significantly since the mid-1980s. These changes include the relative size and sophistication of airline operations, the carriers involved (especially the dominant industry operators), the aircraft fleet mix, and the industry's relationship with the large commercial air carriers in the national air transportation system. Three distinct, but interrelated, trends have provided the basis for the changing character and composition of the industry since the mid-1980s. They are industry consolidation/integration; industry concentration; and the advent of the regional/commuter "jet age."

The most significant change in fleet composition will result from the integration of large numbers of regional jet aircraft into the fleet, most of which occurs in the 50 to 70 seat category. These aircraft have already increased public acceptance of regional airline service, and offer the greatest potential for replacement service on selected jet routes.

The commuter industry went through an even more dramatic change with the advent of the regional jet. Bombardier Aircraft Company introduced the regional jet in the early 1990's. This aircraft, the CRJ-200, was a converted corporate jet capable of carrying 50 people and flying longer commuter legs (up to 800 - 1,000 miles). The regional/commuter fleet, once composed primarily of piston and turboprop aircraft, is moving toward a fleet predominantly made up of regional jet aircraft. The introduction of the regional jet into the dynamics of the demand for air transportation services has significantly expanded the role and market presence of the regional/commuter industry. The phenomenal customer acceptance of the regional jet, coupled with the success operating carriers have experienced in markets where the aircraft is deployed, positions its operators to move beyond the current boundaries of traditional regional/commuter markets. The regional jets' range and speed has opened up new opportunities, allowing regional/ commuter carriers to serve longer-haul markets and to by-pass congested hub airports by providing point-to-point service.

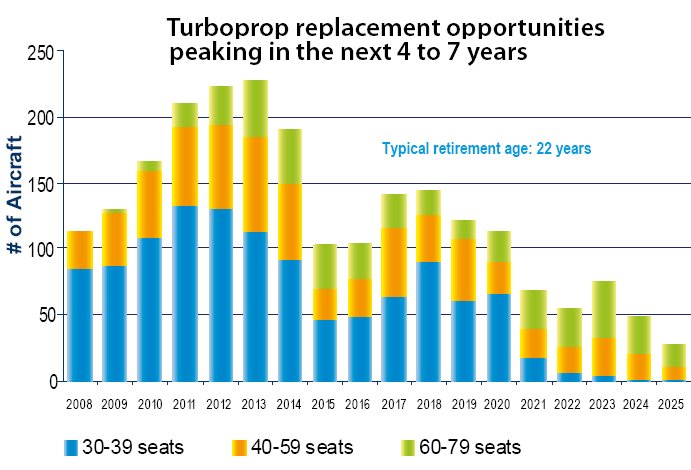

Plentiful and continuing supply of airplanes in the 7,500 to 18,000 lb design payload category: EMB-120, ATR-42 and -72, SAAB 340, etc. airplanes are currently available at attractive prices, having been removed from service and stored as regional passenger carriers move to jets. A continuing supply of these airplanes over the next few years is assured by the ongoing trend toward jet equipment by regional airlines. Because of their popularity (and certain unique capabilities) significant numbers of DHC-8-series aircraft have not yet appeared on the used market at prices compatible with all-cargo conversion - although they too will eventually become available.

As the regional airline market developed, the airlines found that they had to turn to foreign-built aircraft. The US aircraft manufacturers had spent all their time building larger aircraft. In 1986, Boeing Aircraft bought out DeHavilland of Canada and entered the turboprop manufacturing business.

|

NEWSLETTER

|

| Join the GlobalSecurity.org mailing list |

|

|

|